3Q 2017

Click image to enlarge

economy and stocks strong

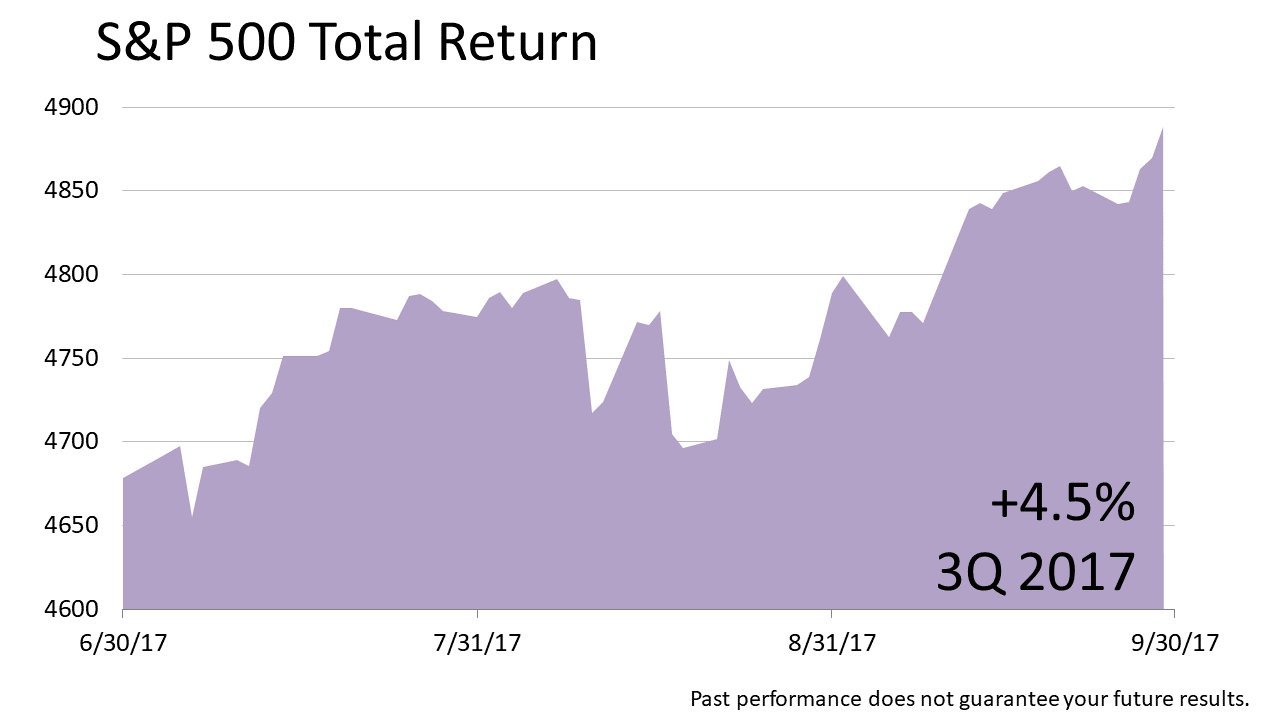

The S&P 500, a key to growth of capital in broadly diversified portfolios for the long run, posted a 4.5% return in 3Q2017, following a return of 3.1% in 2Q2017 and 6.1% in 1Q2017. Total return on the S&P 500 since 1926 has averaged about 10%, making the 9.3% return in the first half of 2017 an exceptionally strong start to the year.

Click image to enlarge

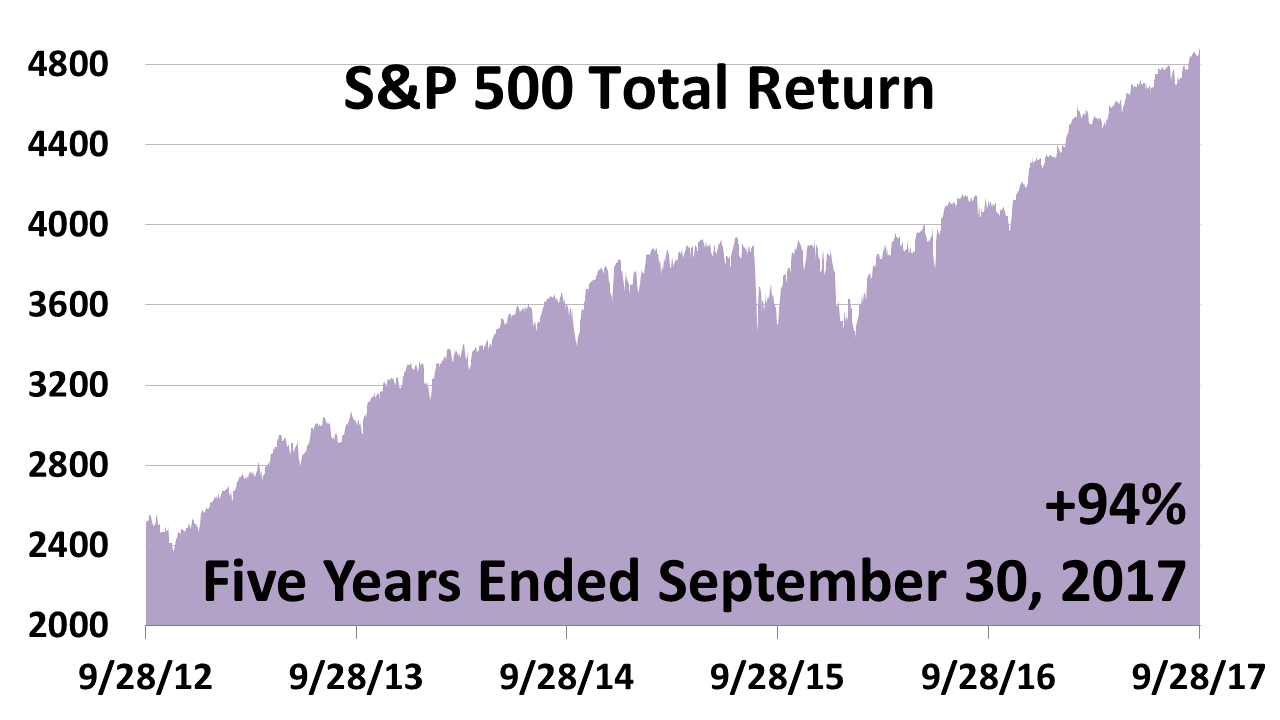

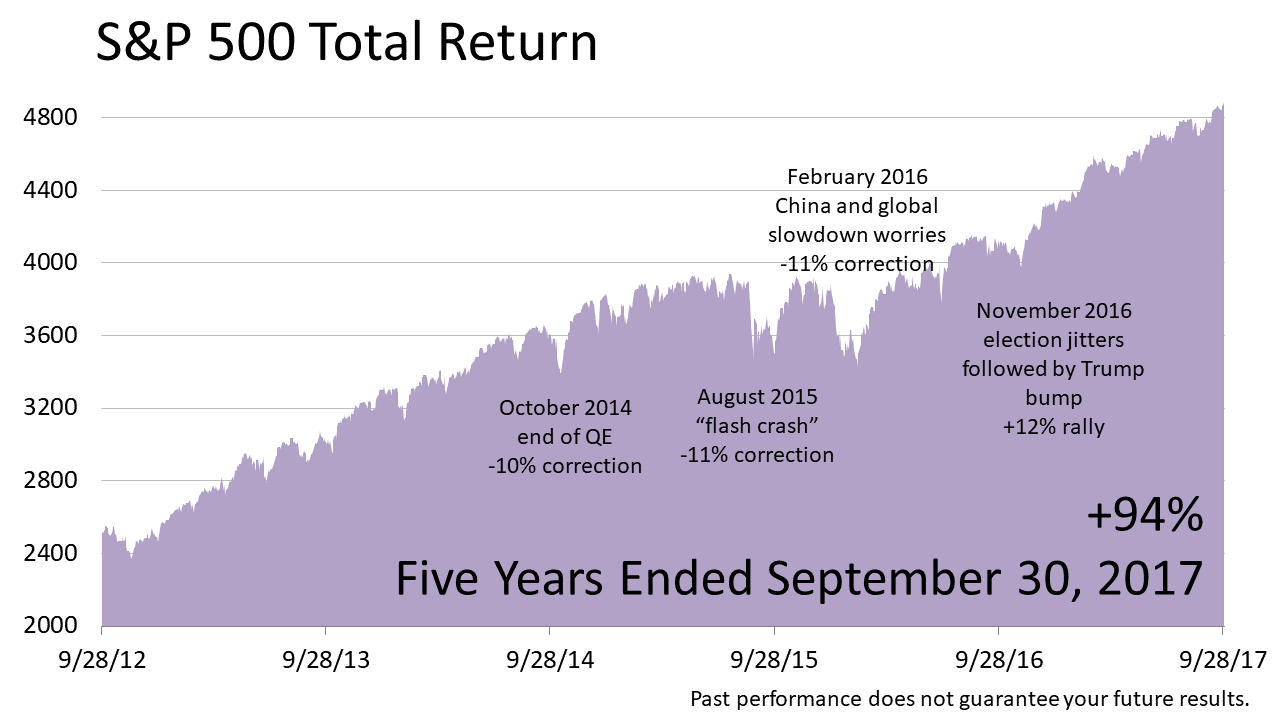

stocks nearly doubled over five years

As this long bull market grows older, the likelihood of a bear-market drop of at least 20% increases. But fundamental economic conditions accompanying bear markets in the past are not present now. Fed policy is not restrictive, GDP growth isn’t slowing, and stock investors are not acting irrationally exuberant.

Click image to enlarge

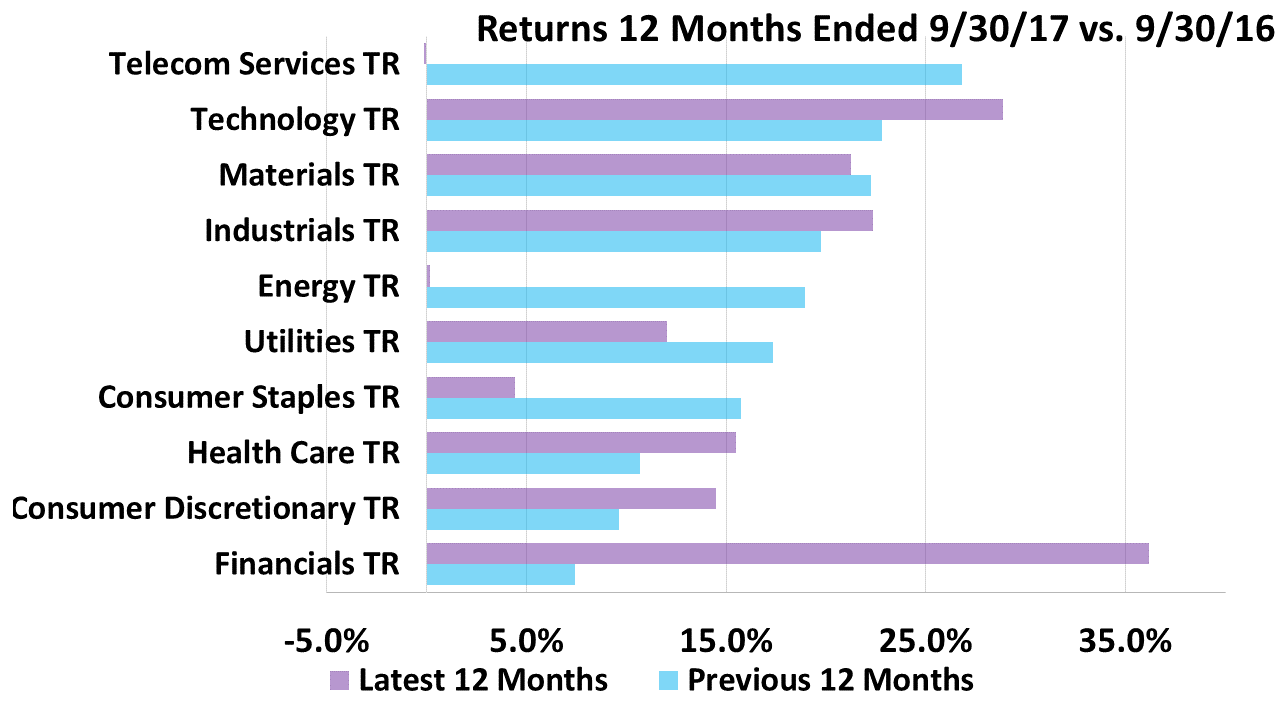

about-face in financials and telecom

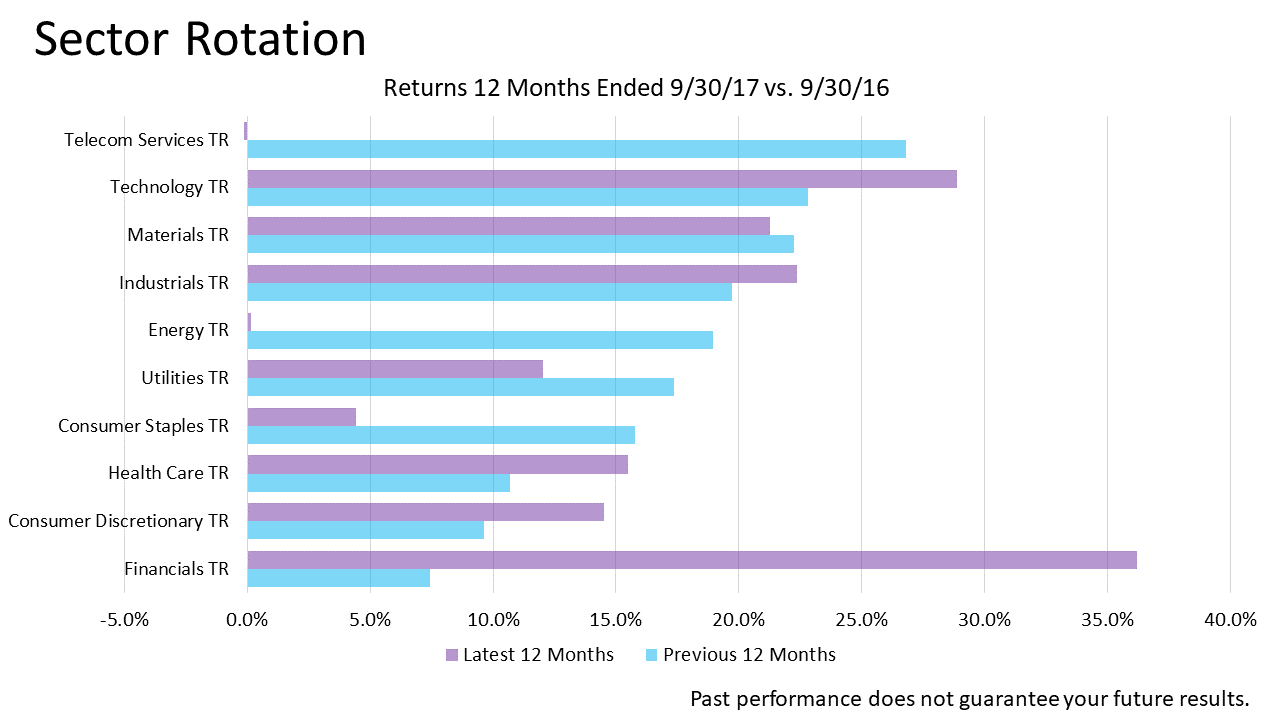

For the 12 months ended Sept. 30, 2017, telecom shares went from darlings to dogs. The last 12 months were an about-face from the prior 12 months. Rebalancing is a statistical approach to managing the risk inherent in sector rotation.

Click image to enlarge

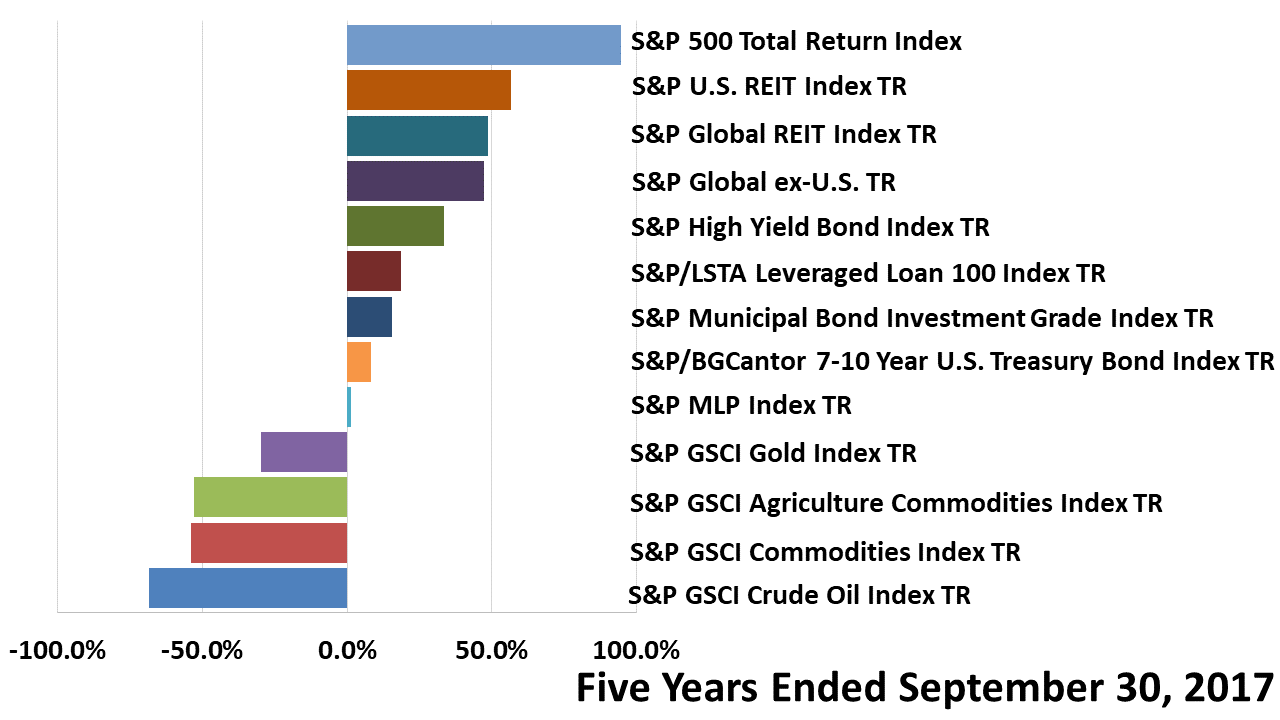

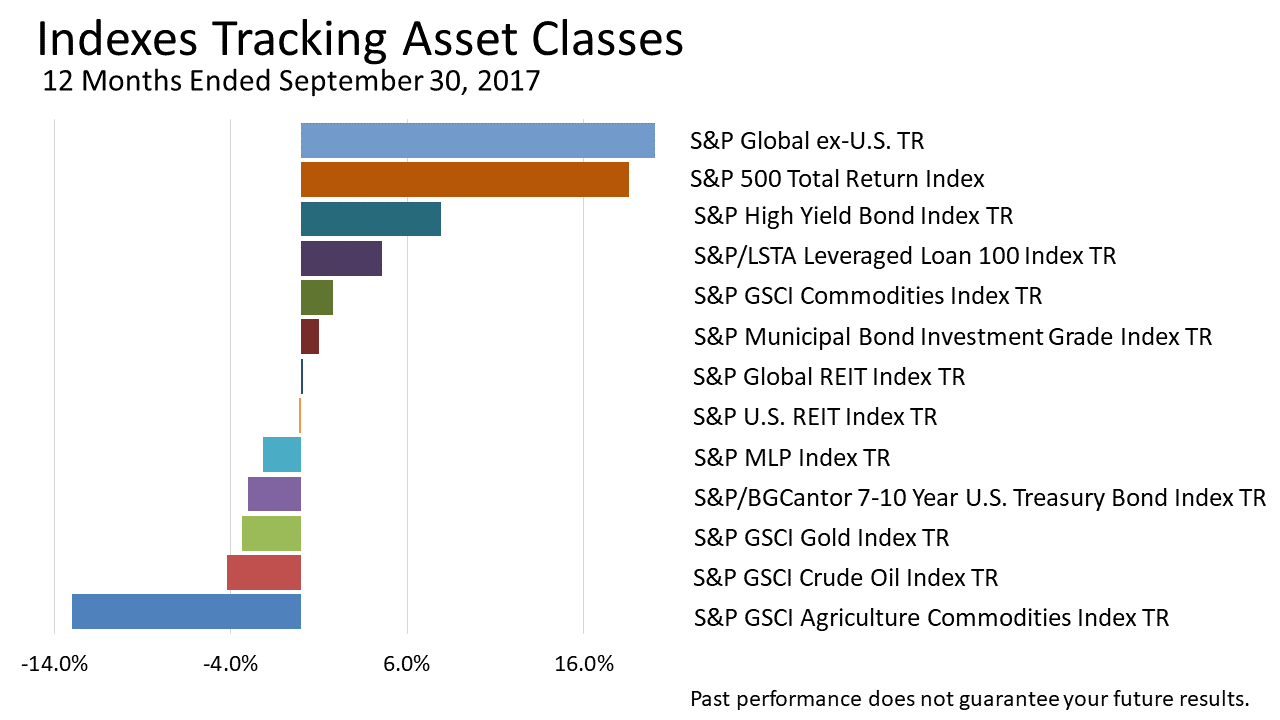

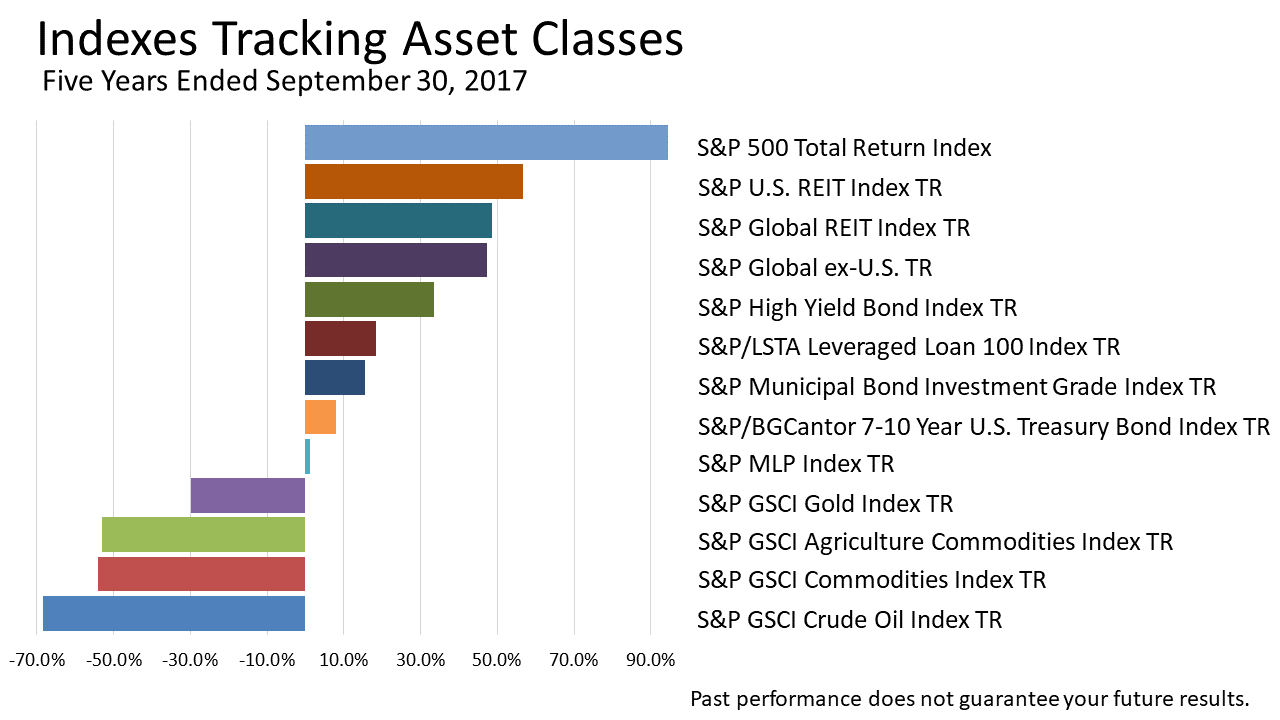

indexes tracking 13 asset classes

A 68.4% loss in the index tracking crude oil’s price in the five years ended Sept. 30, 2017 shows the risk of investing too much in one industry, asset class or style. Among this broad array of 13 asset classes, U.S. stocks came out way ahead in the five years. In recent months, however, foreign stocks outdid U.S stock indexes.

Click image to enlarge

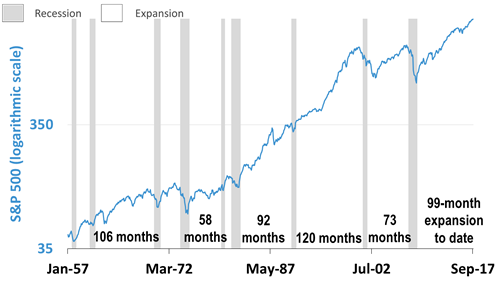

approaching the longest boom

This expansion, which began in March of 2009, is approaching the age of the second-longest boom in modern U.S. history. Unexpected bad news could derail economic growth forecasts at anytime, but this expansion could otherwise yet rival the 120-month boom of the 1990s, the longest post-World War II.

Click image to enlarge

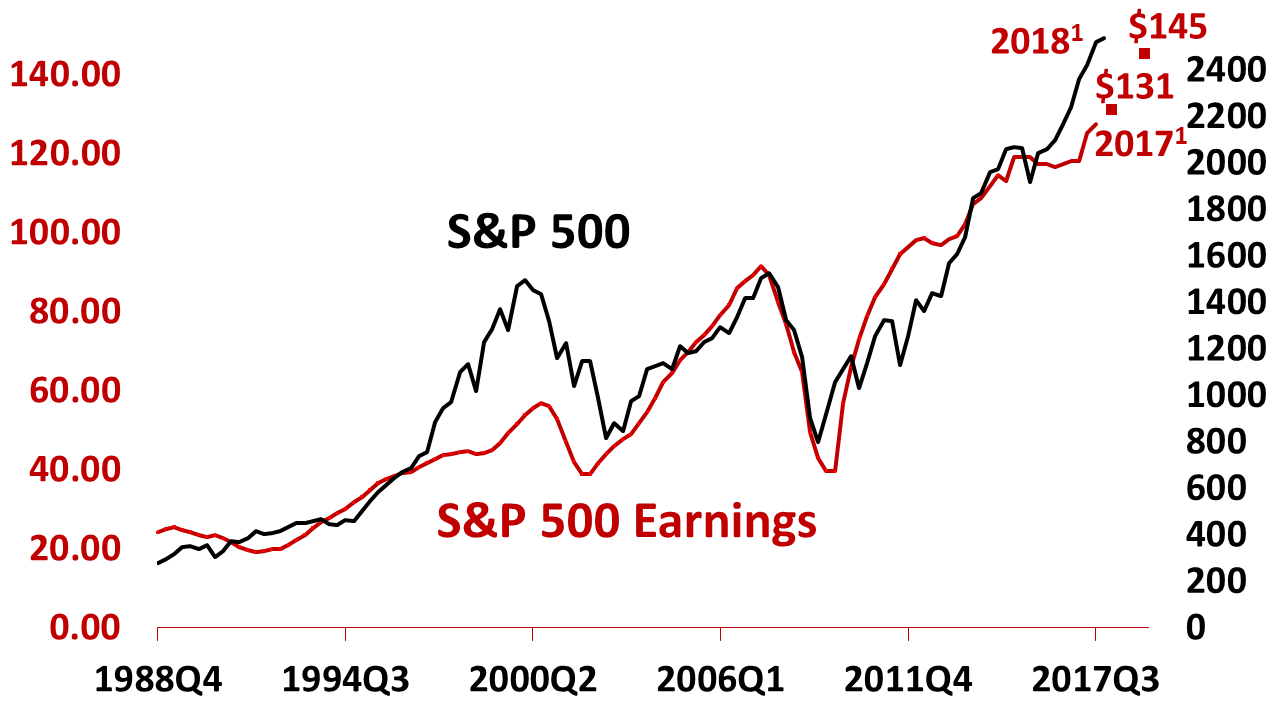

s&p 500 index vs. earnings

Estimated 2017 earnings on an average share in the S&P 500, as of October 2, was $131.12 and $145.45 for 2018. Stocks are not valued outlandishly. In early October, the consensus forecast was for 2.5% growth in the five quarters through September 30, 2018, a big jump in GDP growth, which would be good for stocks.

Past performance of investments is not a very reliable indicator of future performance. Indices and ETFs representing asset classes are unmanaged and not recommendations for any specific investment. Foreign investing involves currency and political risk and foreign-country instability. Bonds offer a fixed rate of return while stocks fluctuate. Leading economic indicators from the Conference Board. S&P 500 bottom-up operating earnings per share for 2016 (actual), 2017 (estimated) and 2018 (estimated) as of July 9, 2017: for 2017, $131.12; for 2018, $145.45. Sources: Yardeni Research, Inc. and Thomson Reuters I/B/E/S survey of consensus estimates. Standard and Poor’s for index price data through October 4, 2017; and actual operating earnings data through 2016.

3Q 2017

Click image to enlarge

Stocks posted a 4.5% total return in the third quarter of 2017, following a return of 3.1% in the second quarter and 6.1% in the first quarter.

Click image to enlarge

Click image to enlarge

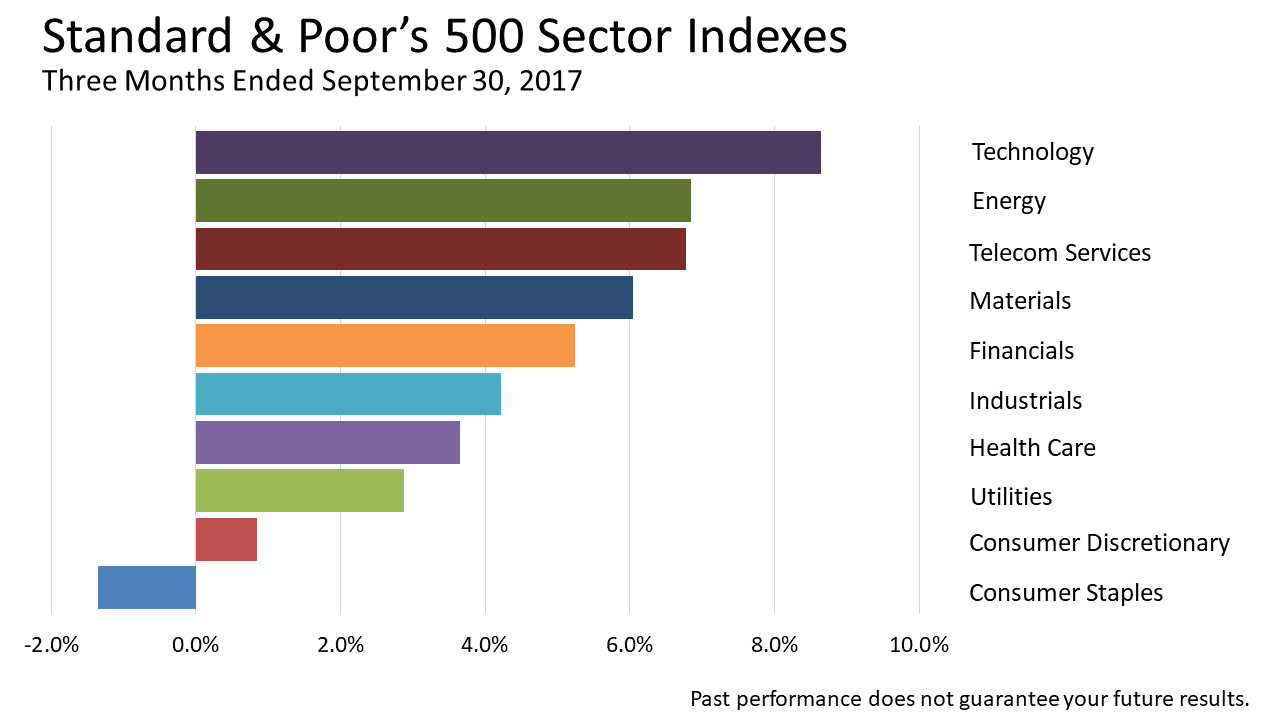

In the quarter that ended September 30, 2017, technology stocks surged. With the price of oil shooting up 10%, energy stocks returned to 6.8%. Defensive sectors driven by consumers languished as investors showed an appetite for riskier assets.

Click image to enlarge

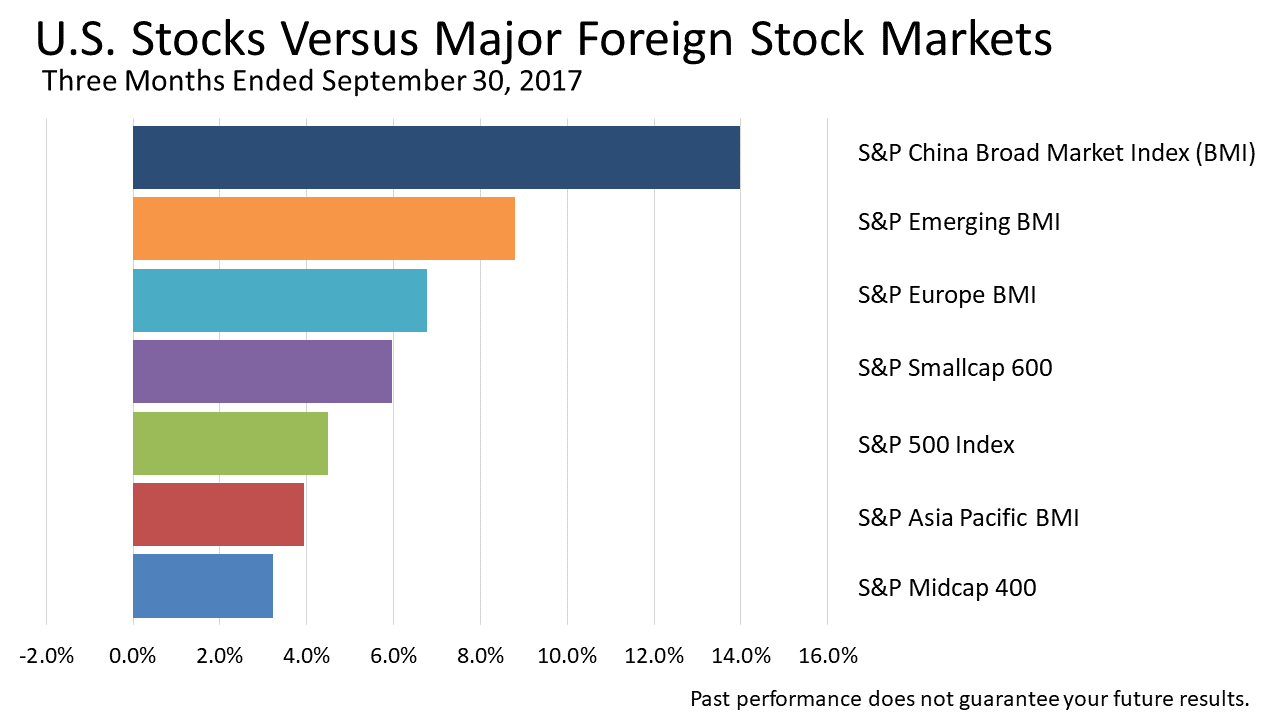

Major foreign indexes again beat the U.S. as global economic growth continued to pick up. This continues the recent trend in which world growth is catching up with the resilient U.S., which led to the global recovery after the financial crisis of 2008.

Click image to enlarge

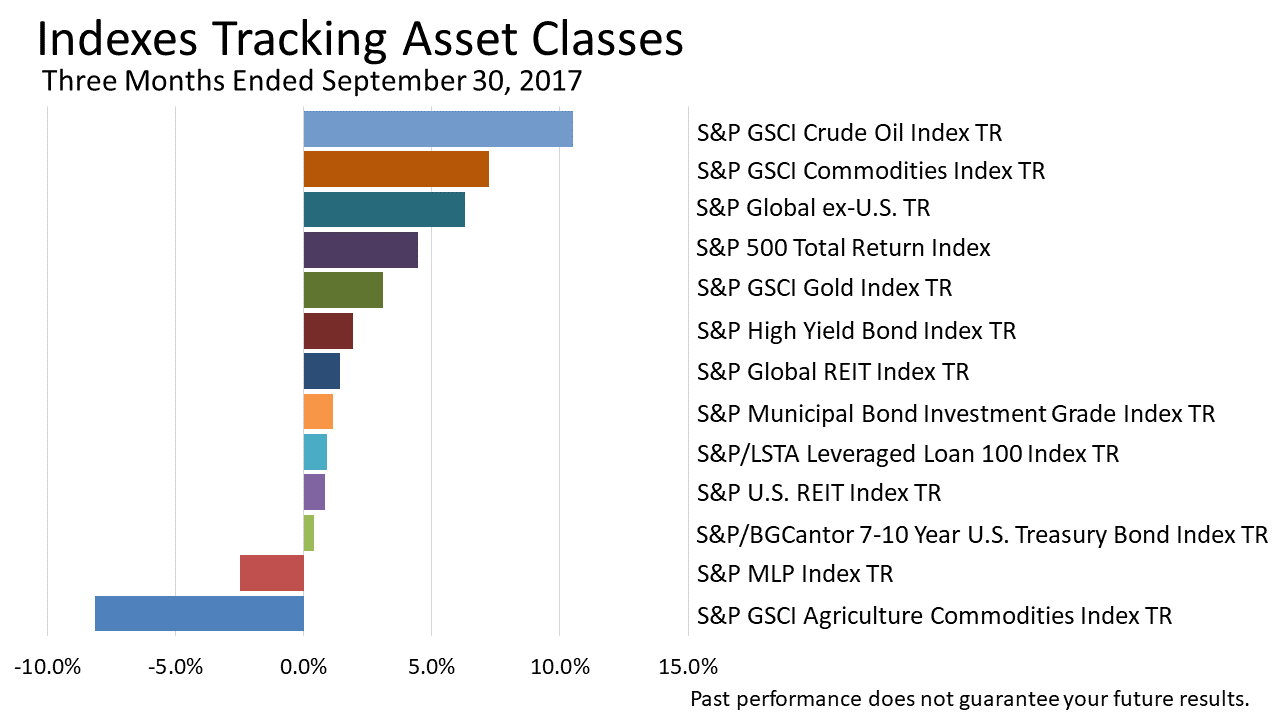

Crude oil's 10% gain following a second quarter slump stands out and non-U.S. stocks again beat U.S. stocks. Fixed-income asset classes all posted positive returns with bond yields stable in the third quarter.

Click image to enlarge

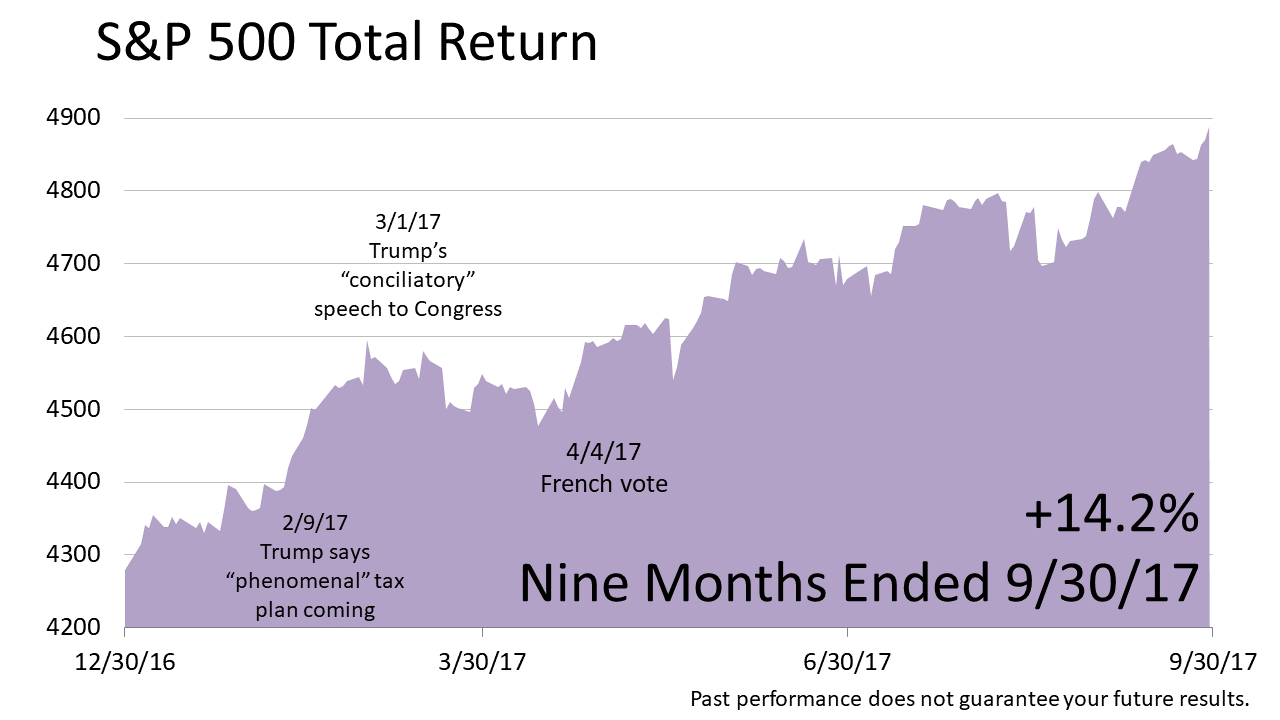

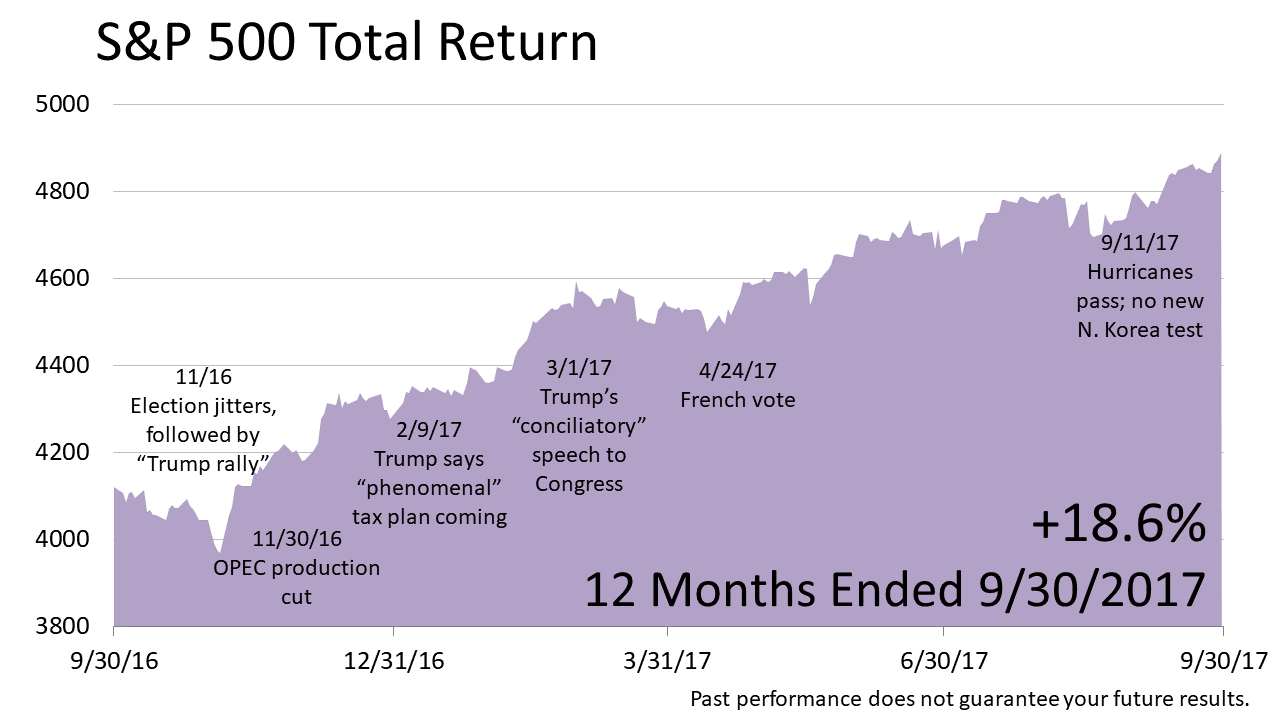

Stocks posted a very impressive 14.2% gain in the first nine months ended in 2017. The year started by continuing a rally that began with the Nov. 8 election of President Trump. Even as investors abandoned expectations that tax cuts proposed by Republicans were imminent, strong economic and earnings data drove stocks to new highs, and global economic growth was additive.

Click image to enlarge

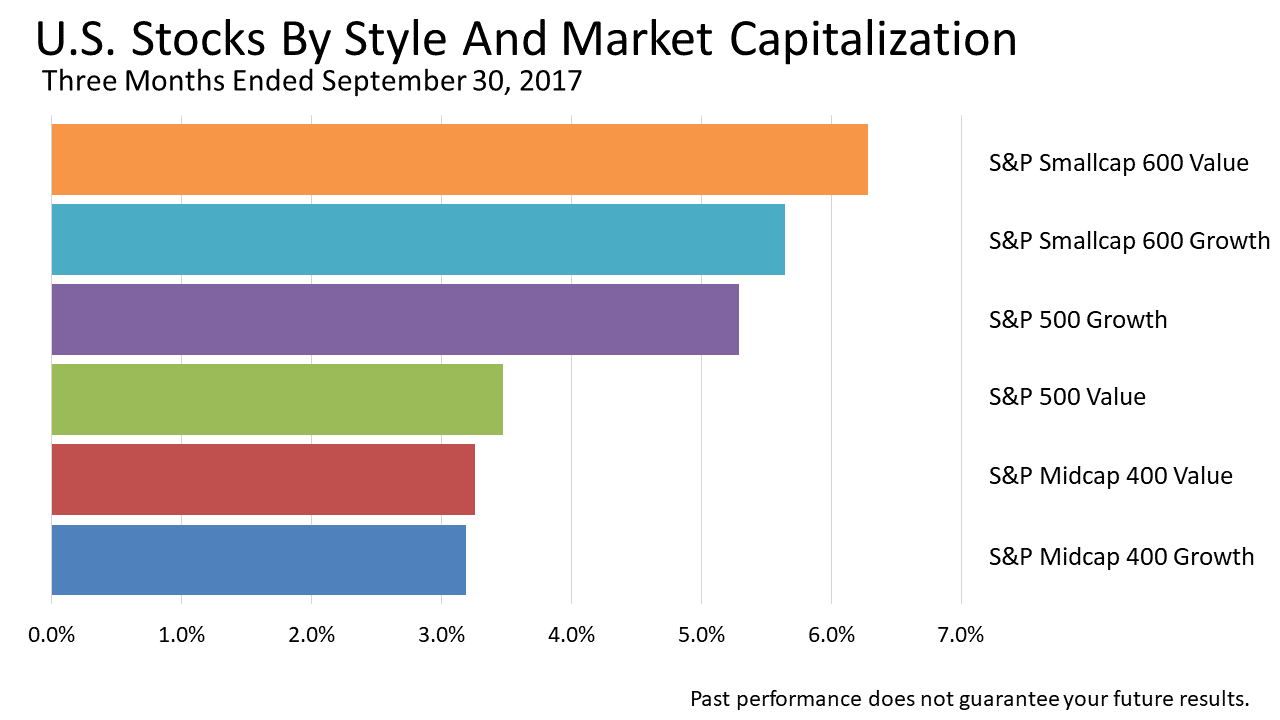

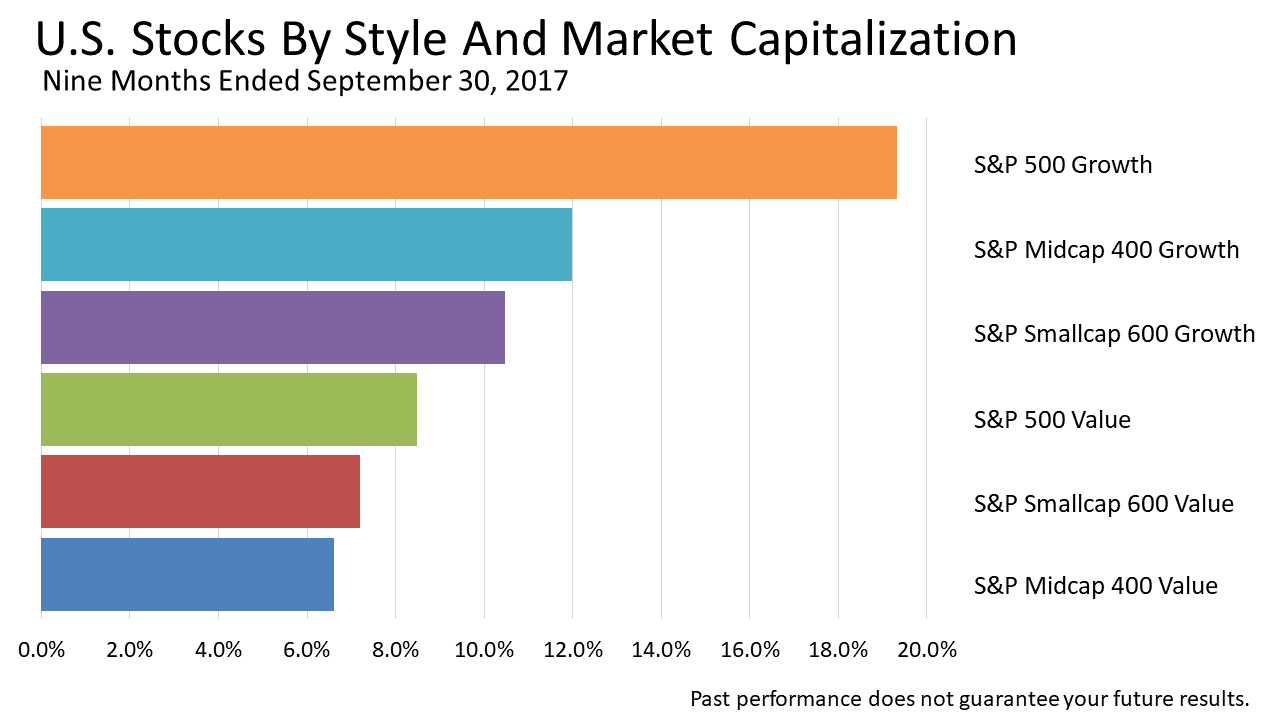

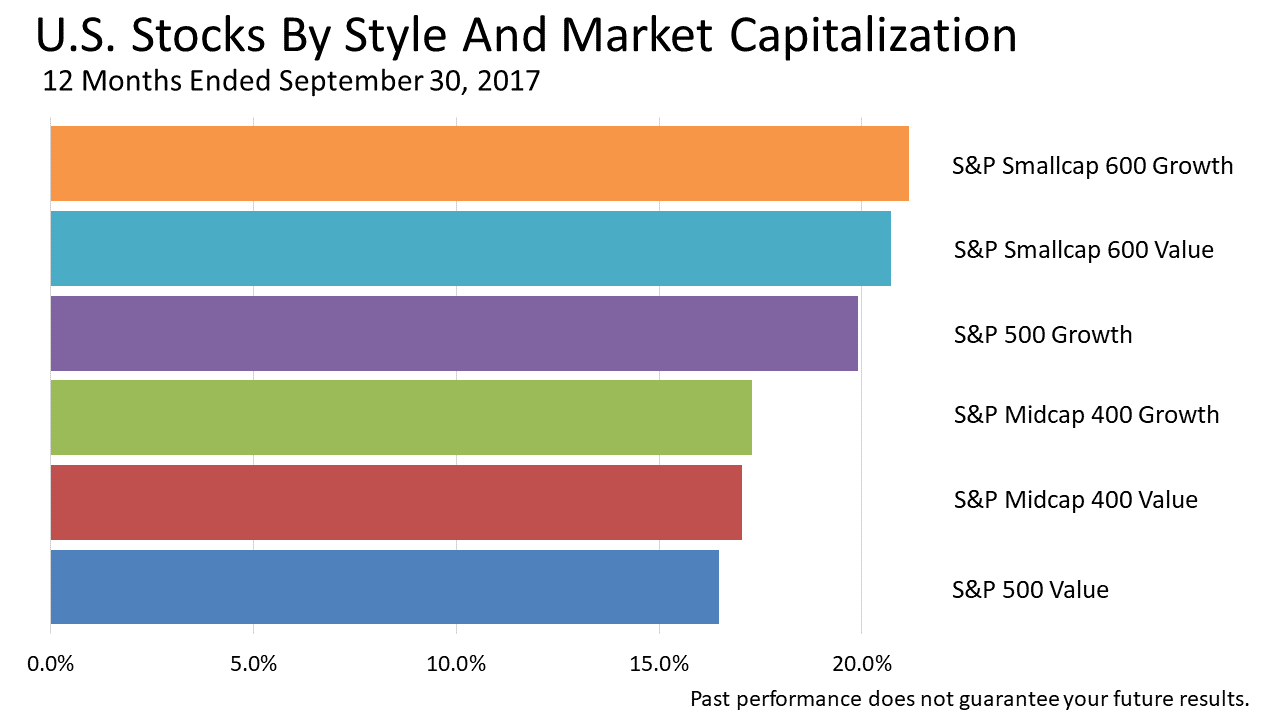

In the nine months that ended September 30, 2017, a wide gap opened between the top-performing large-cap growth stocks' return of 19.3% and the 6.6% on mid-cap value companies. It was the second quarter in a row in which large-cap growth dominated stock classifications. It was the mirror image of the fourth quarter of 2016, when large-cap growth stocks were the laggards. This rotation is not uncommon but defies prediction. It's a dynamic risk methodically tempered by strategic asset allocation and rebalancing.

Click image to enlarge

Technology surged as investors rotated back into the FAANG stocks

Click image to enlarge

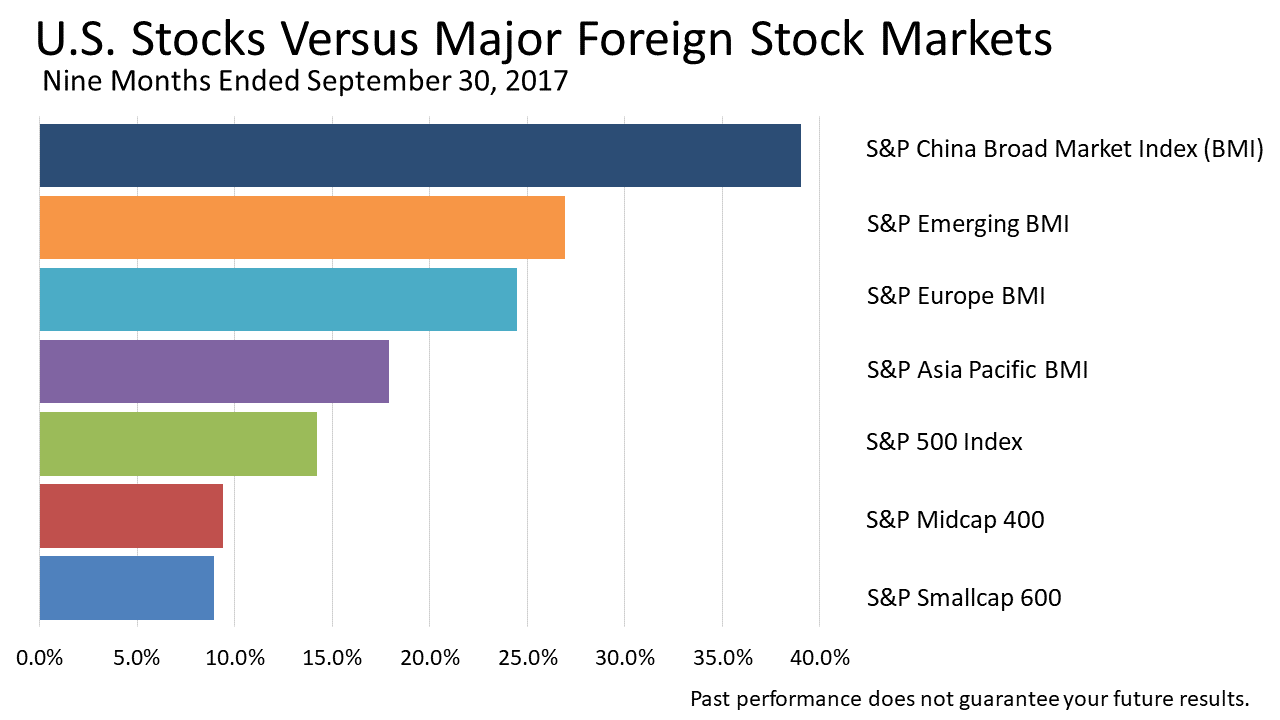

In a reversal from the fourth quarter of 2016 China, Emerging Markets, Europe, and Asia Pacific outperformed U.S. indices in the nine months ended September 30, 2017. Among the U.S. indices, S&P 500 large-caps beat mid

Click image to enlarge

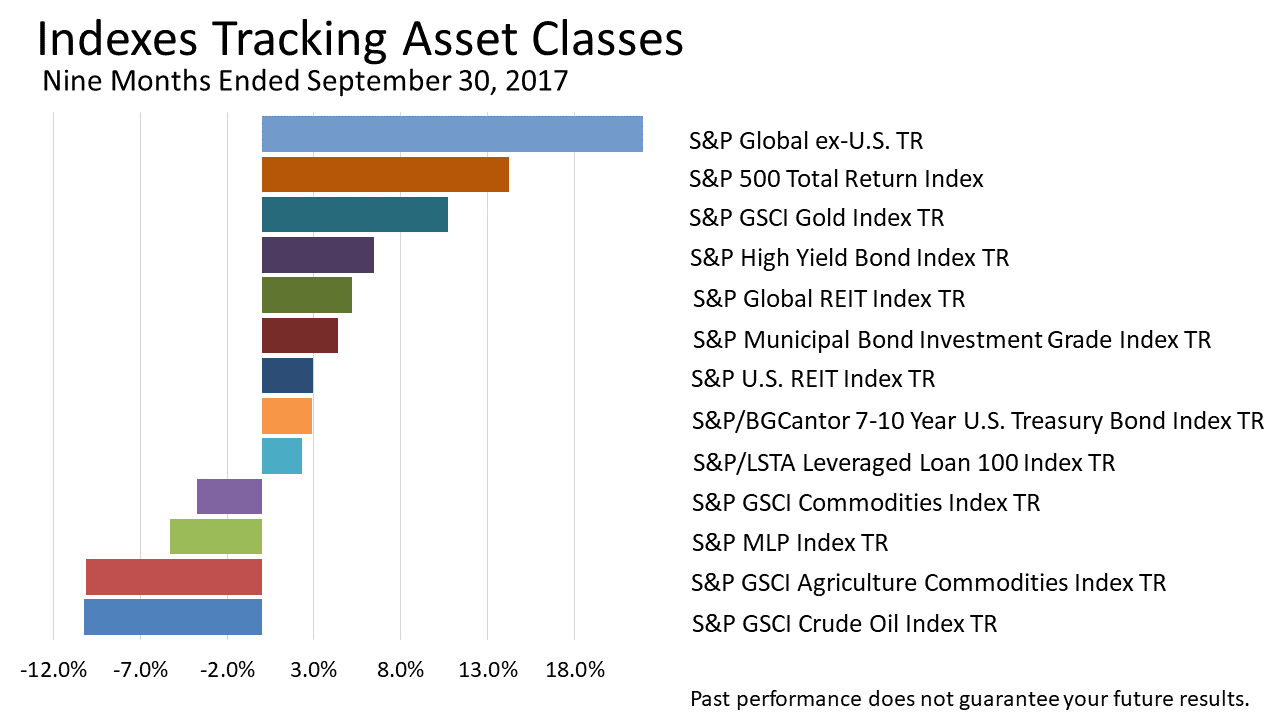

In the nine months that ended September 30, 2017, foreign stocks were No. 1 among the broad array of 13 asset classes shown here. In this period, Standard & Poor's global stock index, which excludes U.S. stocks, gained 22% versus 14.2% on the S&P 500. Overseas markets were catching up with the fourth quarter "Trump rally" in U.S. stocks, as the growth rate of foreign economies improved. Other notable developments include:

- Gold rallied, reversing its fourth quarter 2016 slump on U.S. dollar strength.

- Oil, MLPs and commodities all posted negative returns.

- Riskier assets were rewarded, lifting high-yield bonds and leveraged loans.

- Munis posted additional gains following their fourth-quarter 2016 rallies.

- Across the spectrum of fixed-income assets, returns were positive following a decline in value in income-producing assets in the fourth-quarter of 2016 returns, when bond yields surged and prices dropped post-election.

Click image to enlarge

Stocks over the 12 months ended September 30, 2017 showed a 18.6% total return, as the growth engine of the American investor's portfolios did its job. The long economic expansion that began after the financial crisis of 2008 has shown renewed strength lately. Earnings at the S&P 500 companies recovered from a collapse in the energy and mining sectors. Enthusiasm for a Trump presidency boosted stock prices as 2017 began, and a stream of strong U.S. economic data began to flow amid evidence of global economic acceleration.

An 18.6% return in 12 months is nearly double the historical norm. Does that mean stocks must fall? No. The economy is still strong and earnings are being driven by real-wage growth and strong consumer spending growth, which drives earnings. Of course, past performance does not guarantee future results and market sentiment could send stocks down by 10% or even 15%. Strategically allocating assets based on their long-run history of returns and risk characteristics along with the expected economic environment, is the prudent choice for sensible investors. That means resisting temptation to bet more on stocks after they've risen or selling stocks after prices drop sharply. It means not regretting that you did not own more stocks and staying committed to a long-term strategic plan.

Click image to enlarge

For the 12 months ended September 30, 2017, small-cap companies led the strong rally. Taking more portfolio risk by investing in more volatile types of companies was rewarded with stronger returns. Growth shares generally can be strong performers when the economy is strengthening, as it has been over the 12 months. More conservative types of stocks - like value-priced shares in blue-chips - lagged.

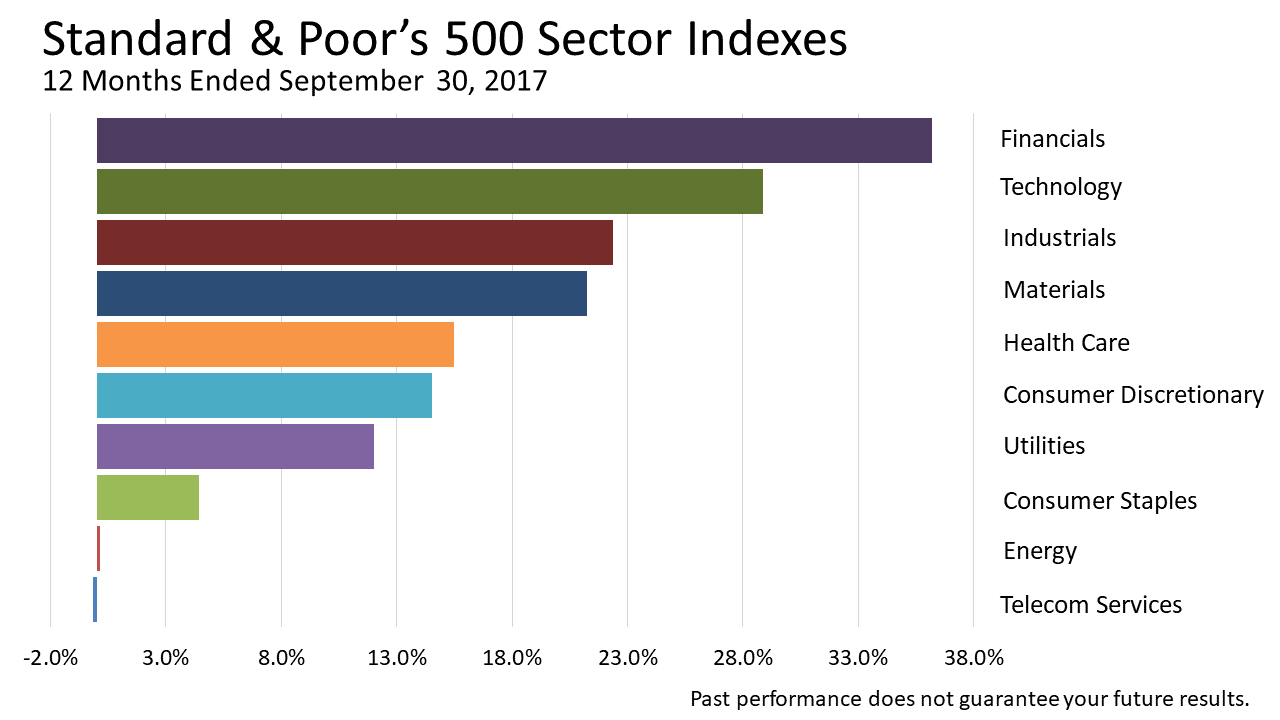

Click image to enlarge

In this snapshot of the 10 industry sectors comprising the Standard & Poor's 500 companies in the year ended September 30, 2017, financial stocks were the biggest gainers. Financial stock prices were bid up on post-election hopes of a significant rollback of Dodd-Frank legislation regulating their activities, along with an expectation that rising interest rates would fatten profit margins at banks.

The lagging sectors during the 12 months - telecom, consumer staples and utilities - are defensive sectors, less volatile and less exciting segments among America's largest publicly-held companies. Investor thirst for risk has grown. In those12 months, energy company shares slumped, as crude oil retraced some of last year's price recovery.

Click image to enlarge

Modern Portfolio Theory suggests periodic portfolio rebalancing as a way to smooth out short-term differences in returns on different types of investments in a portfolio. This chart illustrates how that works, using the 10 industry indexes that comprise the Standard and Poor's 500 companies. It shows an industry's return in the 12 months ended September 30, 2017 compared to its return in the 12 months ended September 30, 2016. For example, telecom stocks showed a flat return in the 12 months through the end of September 2017 after leading all industry sectors 12 months earlier. Telecom shares went from darlings to dogs. The last 12 months were a complete about face from the prior 12 months. Applying a quantitative discipline that expects volatility and rebalances based on these shifting preferences is a statistical approach to managing the risk inherent in sector rotation.

Click image to enlarge

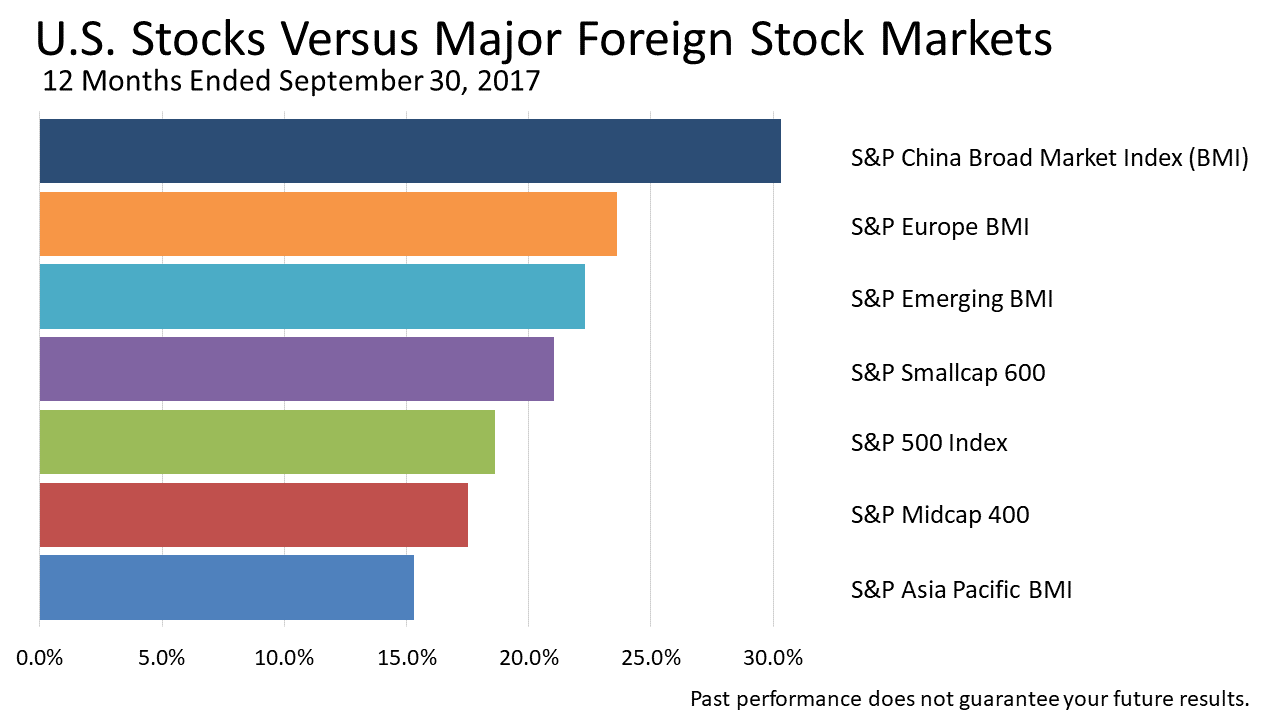

While U.S. stocks posted a booming 18.6% return in the 12 months ended September 30, 2017, foreign stock markets across the globe performed even better, as the economies of China, Europe and Emerging Markets gained strength. The surge of the U.S. dollar in 2014 and 2015, which pummeled the value of foreign stocks in broadly diversified portfolios, has faded from memory. For diversified portfolios, the strengthening of foreign stock returns versus U.S. shares brought a welcome shift in leadership because growth in countries making up the world economy is not a zero-sum game.

Click image to enlarge

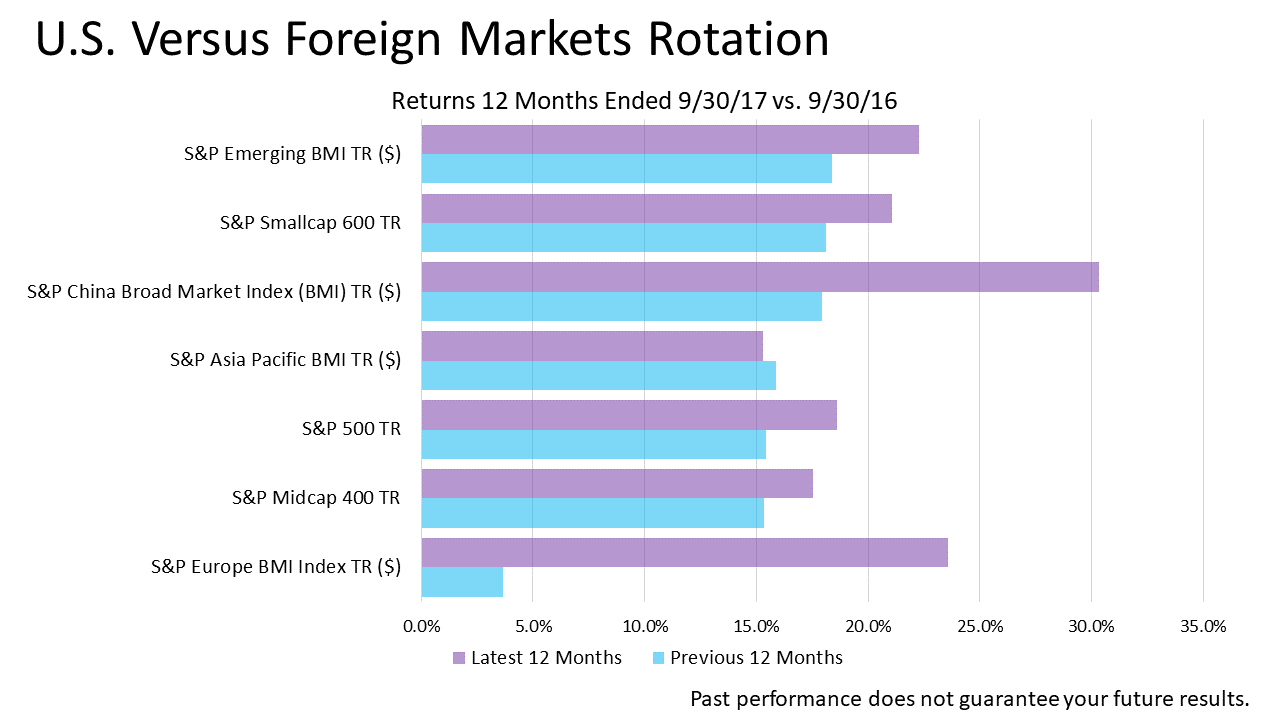

European shares were the worst performers in the 12 months ended September 30, 2016, but outperformed U.S. stocks in the following 12 months. Periodic rebalancing invests in lagging and losing segments of a broad investment universe, forcing purchases of assets depressed based on historical results and expected economic growth. So, if a hypothetical portfolio was rebalanced October 1, 2016, for instance, you would have purchased more shares in the losing European stock market than in the other types of stocks shown. In classic form, the laggards in 2016 came back in 2017. European stocks 23.6% return in 2017 was second only to China's highly-volatile stock market's return of 30.3% in the 12 months ended September 30, 2017.

Click image to enlarge

In the 12 months that ended September 30, 2017, non-U.S. stocks were the top asset class. Global economic growth picked up, boosting foreign investments. Laggards during much of the recovery that followed the global economic crisis, foreign markets are playing catch up with U.S. stocks, even as U.S. stock returns astound. Stock markets everywhere have been surging on the strength of a synchronized global expansion, outperforming every other asset class by a wide margin. Oil, gold and commodities were the laggards for the period, as crude oil prices gave back some of their 2016 gains.

Click image to enlarge

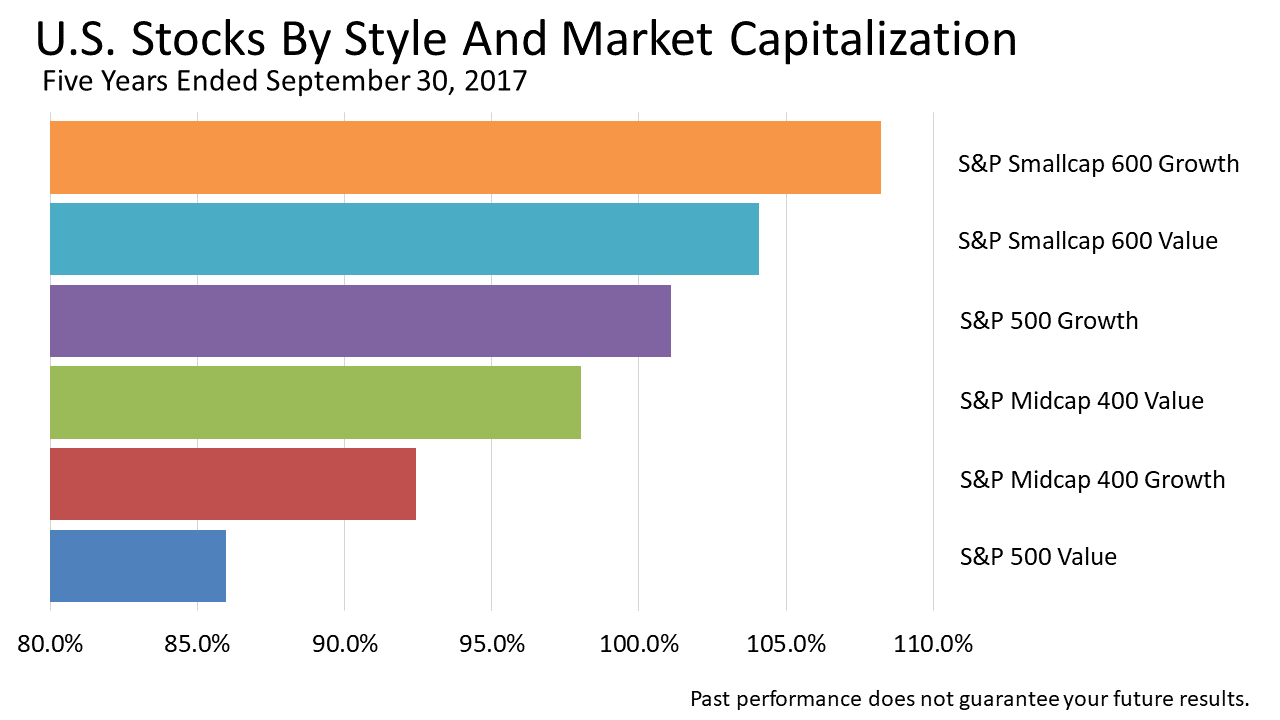

Over the five years that ended September 30, 2017, small-caps were No. 1 among major U.S. stock asset-class styles. More volatile companies - small-caps, which are subject to bigger swings in price than large companies - gained more than other asset-class styles.

Small-cap outperformance reflected growing confidence in the economy and greater tolerance for risk, as expectations brightened for U.S. and global economic strength through 2018.

Click image to enlarge

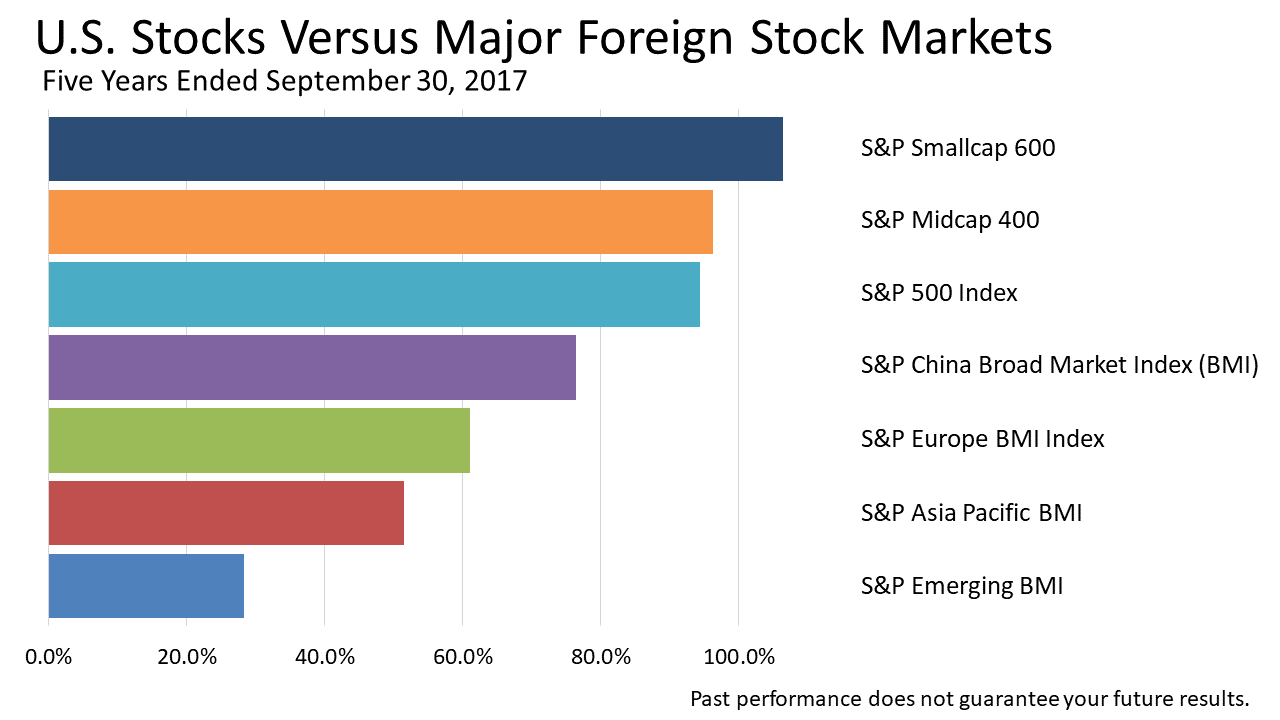

For the five years that ended September 30, 2017, U.S. stock indexes outperformed the rest-of-world by a substantial margin, despite a surge in equities in non-U.S. markets in the last 12 months.

Also, among the U.S. indexes, note that small and mid-caps returned more than the large-cap S&P 500 index. This is, in fact, the long-term norm. Slightly better returns are expected over the long-term for tolerating slightly more volatility of returns on small and mid-caps compared to large-caps.

Click image to enlarge

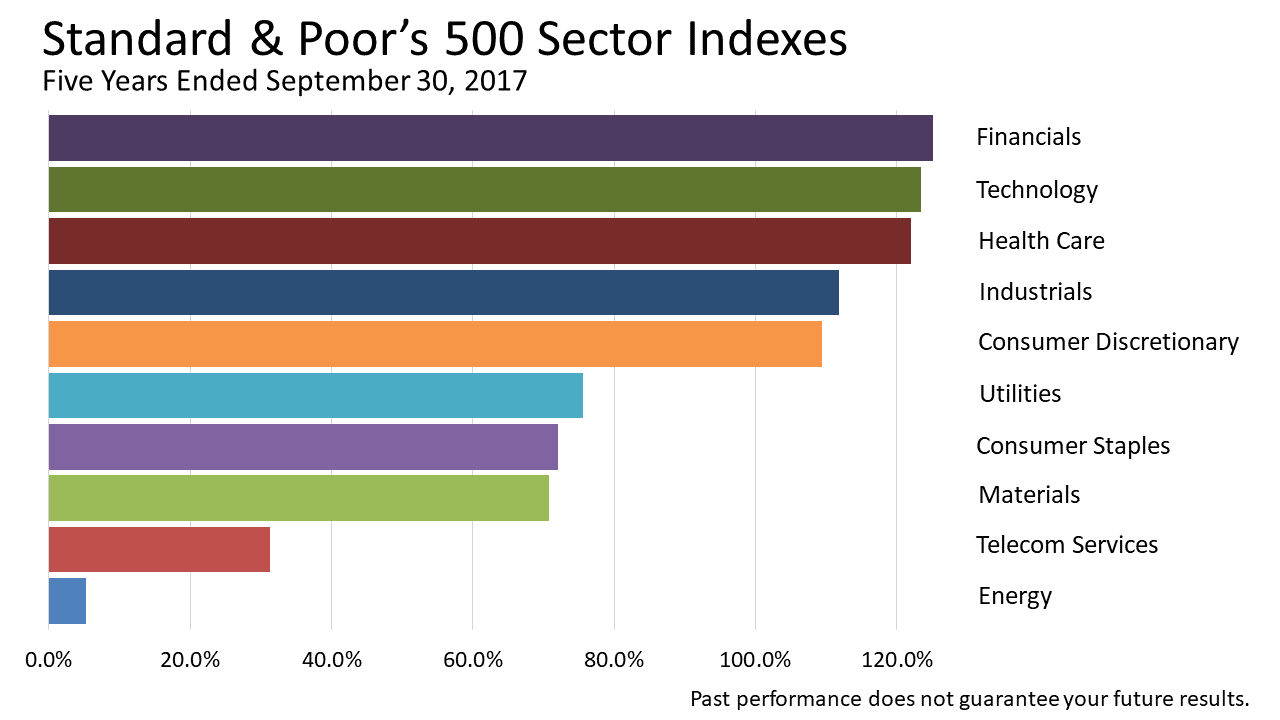

For the five years that ended September 30, 2017, value-oriented industry sectors lagged. Consumer staples, energy, raw materials, telecom, utilities and consumer staples where didn't give investors the appreciation or growth sectors. Companies with earnings growing fast relative to peers were bid up higher in price.

The No. 1 industry over the five years was financial services. Some large financial services companies literally collapsed in the 2008-09 global financial crisis. The return of financials to the No. 1 slot for a five-year period represents an indication that the economy's most damaged sector is fully recovered.

A massive change in the way information is consumed set big-tech aloft. Facebook, Amazon, Apple, Netflix and Google were bid up and fully valued.

Energy and material sectors were slammed by the collapse in the price of oil and other commodities. The energy sector of the stock market is highly correlated with crude oil prices. The price of crude oil, even after almost doubling from its early-2016 bottom of $26 per barrel, as of mid-October 2017 remained priced at less than half its 2014 peak in price of $114 per barrel.

Click image to enlarge

While U.S. stocks are the key growth engine in diversified portfolios, stocks are only one part of a prudent portfolio.

This chart shows the five-year returns on a broad set of indexes representing 13 asset classes, including the S&P 500.

The 68.4% loss in the S&P Goldman Sachs index tracking crude oil's price gives you a clear indication of the risk of investing too much in any one industry, asset class or style.

Real returns were strong in this five-year period, which was characterized by a remarkably low inflation rate of less than 2%.

The Standard and Poor's 500 showed a total return of 94%, double the return of major foreign stock markets.

America led the world economy out from the server recession that followed the 2008 financial crisis.

The U.S. bounced back before, and more, than any other major world economy after The Great Recession and this five-year period is replete with evidence of American exceptionalism.

It's actually pretty amazing.

At the bottom of the pack, in last place among the 13 asset classes shown, was crude oil.

The price of oil dropped globally because of a surge in U.S. supply that resulted from the shale-fracking revolution.

Some economists say oil prices won't ever recover back to $100 a barrel because U.S. oil production would increase and fuel lower prices.

Commodities and gold were losers over the five years, due to the strength of the dollar, slowing demand for most commodities and low inflation.

Click image to enlarge

The five-year period is part of a bull in stocks that started in March 2009, as the economy emerged from the worst financial crisis in decades.

After rising steadily in 2012 and 2013, the Standard & Poor's 500 traded sideways from mid-2015 to mid-2016, nosediving three times along the way, share prices broke out after the November 2016 election and they've climbed steadily since then.

The expansion is now the second longest in modern U.S. economic history.

Over the last five years, the S&P 500 total return, which includes reinvestment of dividends, was 94%.

Without dividends, the average price of a share in the S&P 500 soared by 75%.

The Standard & Poor's 500 has been breaking new all-time highs for months, and stocks are trading near the high end of their historical valuation range.

Larry Fink, the CEO of the world's largest investment manager, recently issued a warning about the stock market.

As this long bull market grows older, the statistical likelihood of a bear market - a drop of at least 20% - does indeed increase.

But fundamental economic conditions that have accompanied bear markets in the past are not present at this time.

We're not seeing restrictive Fed policy. Economic growth isn't slowing. Stock investors are not acting irrationally exuberant.

A correction of 10% or 15% is always possible, just on a change in sentiment or unexpected bad news.

Yet the economy shows no signs of coming undone in the foreseeable future, and the bull market could also go on longer and head much higher.

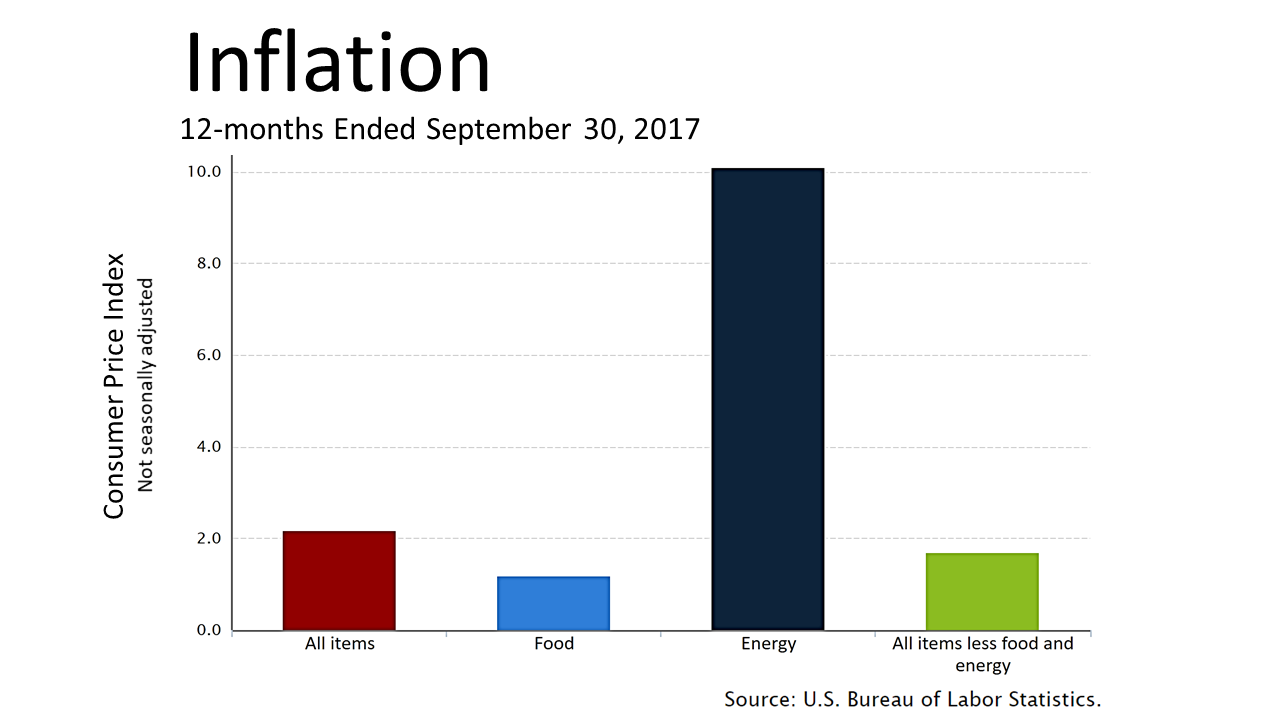

Click image to enlarge

All recessions in modern U.S. history have been caused by the Fed, usually because the Fed tightened credit too much to squelch inflation.

In the current economy, inflation has been below normal and lower than expected.

That's giving the Federal Reserve added leeway to let the economy run faster without worrying about igniting inflation.

The latest numbers from the government showed that oil prices rose in September because of the disruption from hurricanes hitting the Gulf Coast, but inflation otherwise remained benign.

Click image to enlarge

While stocks are really fun to talk about in the midst of a long-term economic expansion that is accelerating, the fourth quarter of 2017 is a time to focus on year-end tax planning.

While the fourth quarter is always when you focus on year end planning, this year the stakes are higher.

The U.S. Tax Code may undergo its most significant revision since 1986.

You don't want to ignore what's proposed and risk making a costly financial mistake.

Click image to enlarge

Two Congressmen, two Senators and two Trump administration officials published a framework on September 19th for a 10-year tax cut totaling $1.5 trillion.

Then, the Trump administration, on September 27th, published a nine-page outline for cutting taxes over the next decade by about $2.2 trillion.

Click image to enlarge

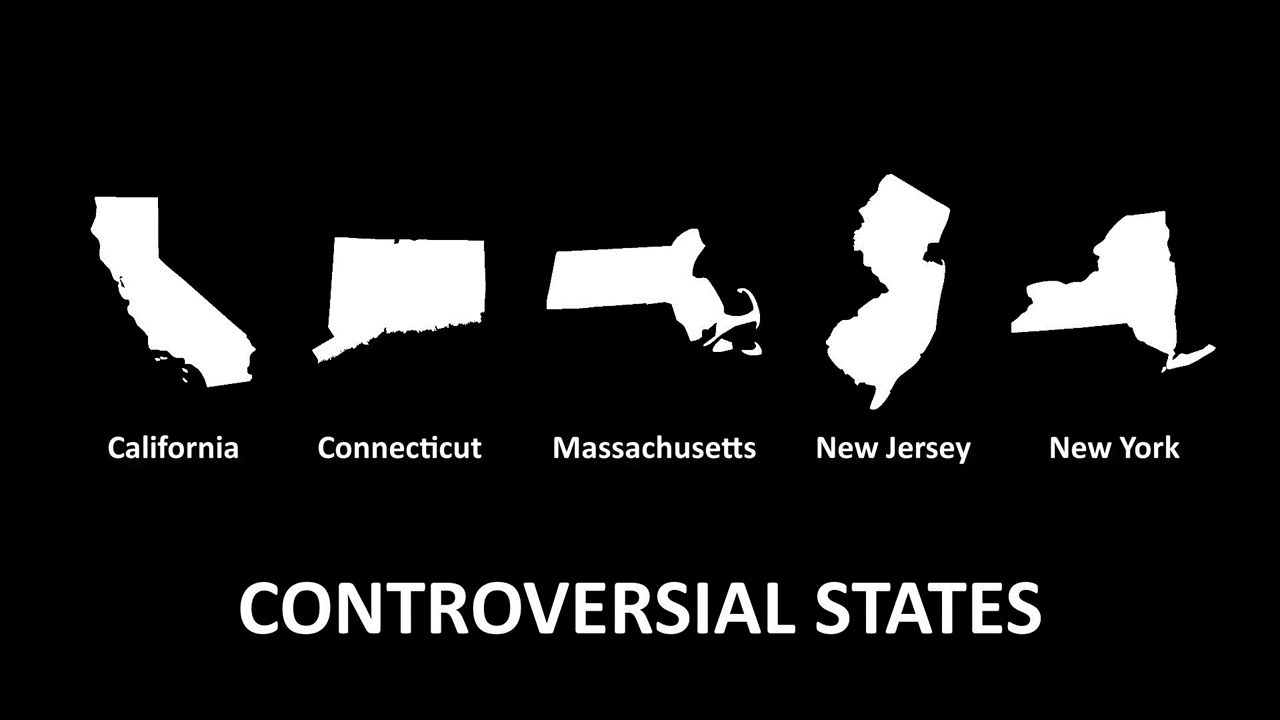

The President's proposal eliminates the federal deduction for state and local taxes.

This single provision raises about $1 trillion of revenue over the next decade and is key to paying for the tax cut.

Places with relatively high state and local taxes - California, Connecticut, Massachusetts, New Jersey and New York - are expected to fight this change.

Click image to enlarge

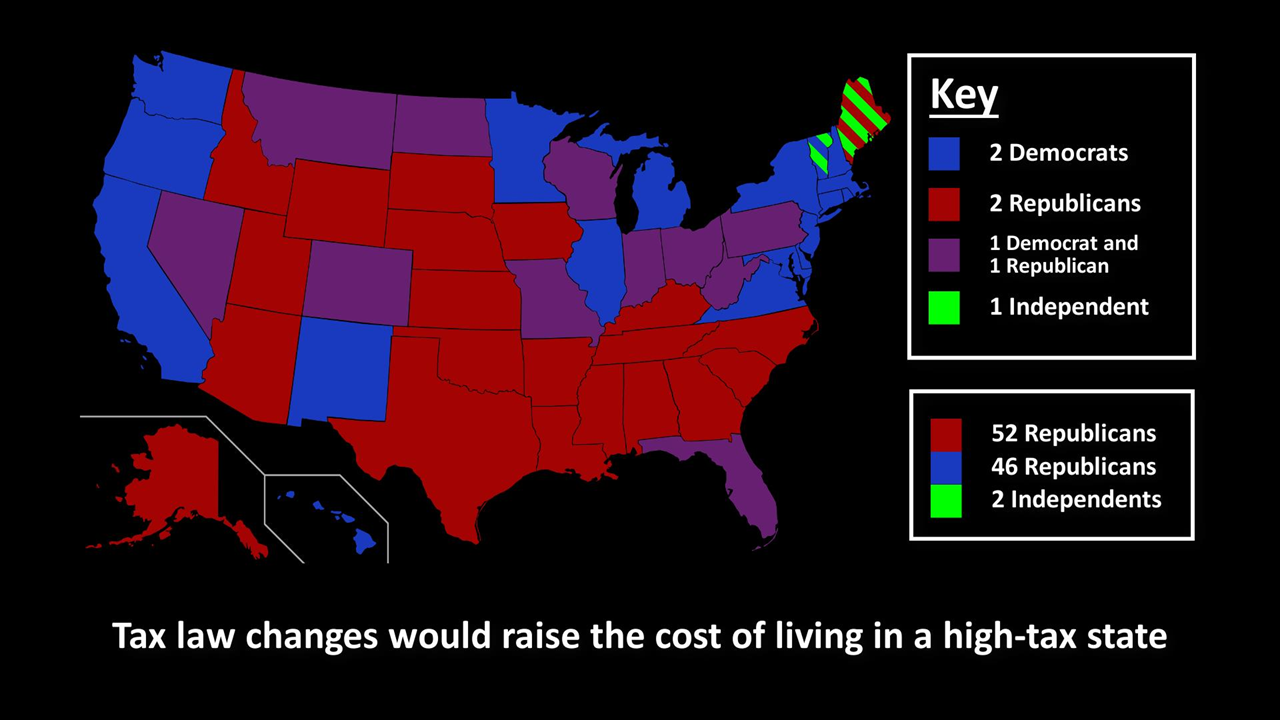

Since those states have Democratic Senators, this provision could pass in the Senate - assuming all Republicans vote along party lines - but its survival in the House of Representatives is less certain.

This change to the tax law would effectively raise the cost of living in a high-tax state.

As a result, residential real estate values in these high-tax urban and suburban areas would be likely to fall.

It would lower the nest egg of millions of pre-retirees and retirees in these places.

The success of this single provision will largely determine the ultimate size of the final tax cut package, and we will follow its success in the weeks ahead.

Click image to enlarge

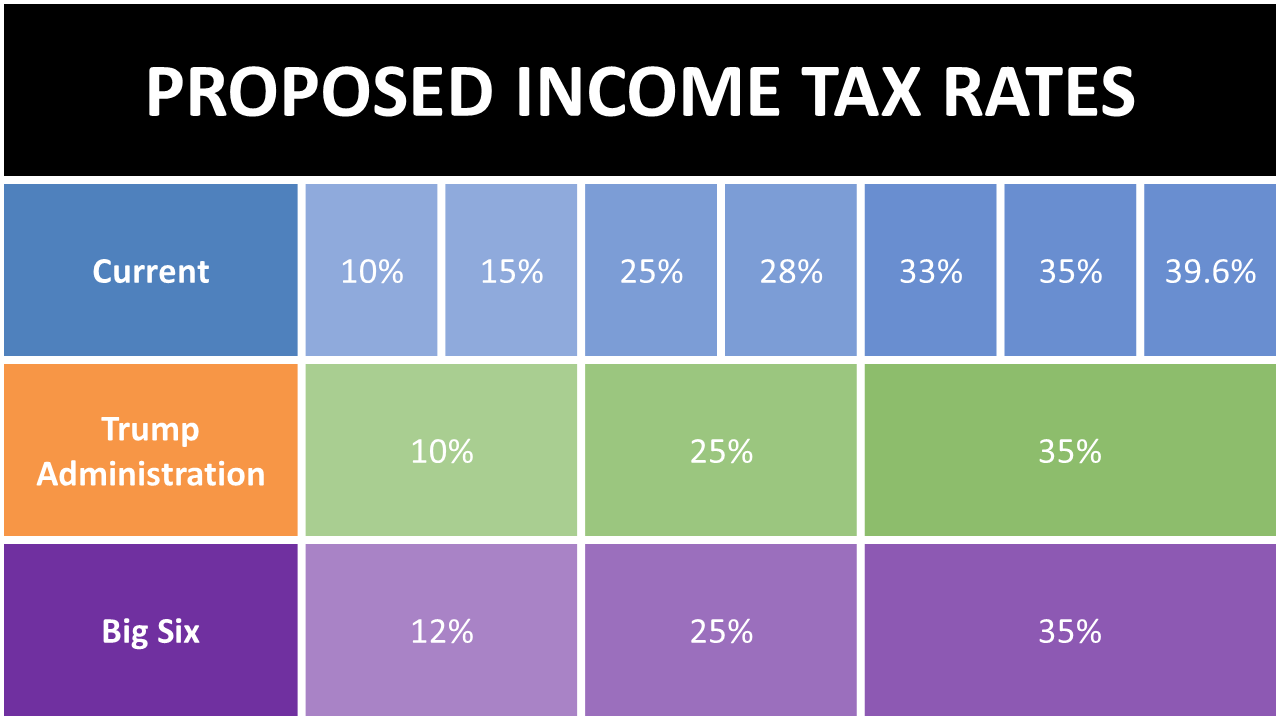

Year-end tax planning is all about timing your deductible expenses and income, and that's all the more important right now because your tax rate may be much lower next year.

Under the proposal, we go from the seven current tax brackets to just three.

This proposal would simplify taxation and crush the tax preparation business.

Most itemized deductions will be eliminated and so will the Alternative Minimum Tax - assuming the reform plan becomes law.

Click image to enlarge

This proposal is really good for business owners, doctors, lawyers, and other professionals operating as an S corporation, sole proprietorship, LLC or other form of partnership - if you are in the 35% or 39.6% tax bracket, your tax rate may drop to 25%.

As the year end approaches and the size and shape of tax reform becomes clearer, you want to think about ways of shifting income to 2018 and accelerating deductions.

You may need to find a way to accelerate the purchase of a car, computers or other capital investments into this year.

If your tax bracket is going to drop as a result of the reforms, you may want to take that deduction you've been thinking about this year instead of waiting.

It's also wise to consider deferring capital gains on securities into 2018.

Click image to enlarge

Roth IRA conversions will need to be carefully reviewed in the overall context of tax reform.

Anyone considering a conversion to a Roth IRA from a traditional IRA will likely want to postpone conversion until next year.

Converting next year would be a lot less costly if your tax bracket declines from 35% to 25%.

Click image to enlarge

If you inherited an IRA in 2016 or 2017, you may face some unexpected tax consequences.

The income tax deduction for estate taxes may be eliminated.

While this change won't affect that many people, it's worth mentioning because of the tax savings to be gained from planning.

Click image to enlarge

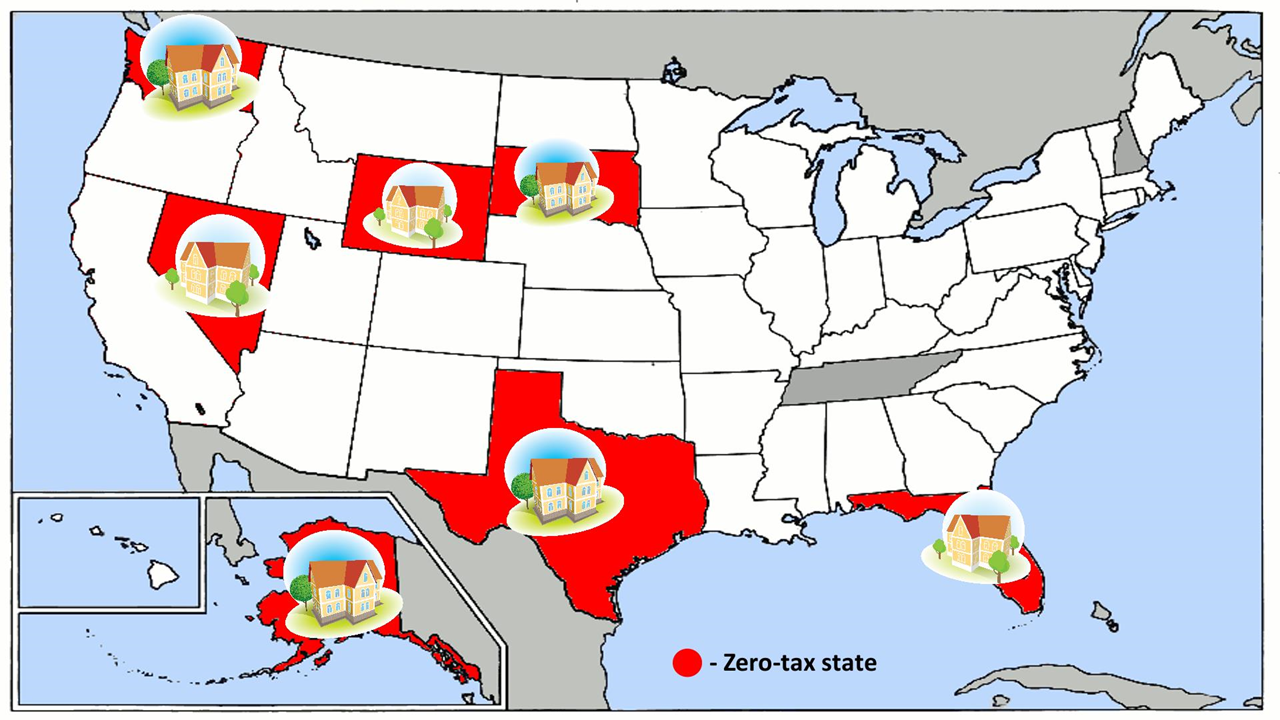

If the proposal to eliminate the federal deduction for state income taxes does indeed become law, creating trusts in zero-tax states will be more important than ever.

Although the estate tax may be eliminated, a trust in a zero-tax state could provide significant annual savings on income taxes.

Click image to enlarge

If you inherited assets in 2016 or 2017, choosing the official date of death for tax purposes could be important.

You'll need to pay close attention to events in the weeks ahead to stay in touch.

Click image to enlarge

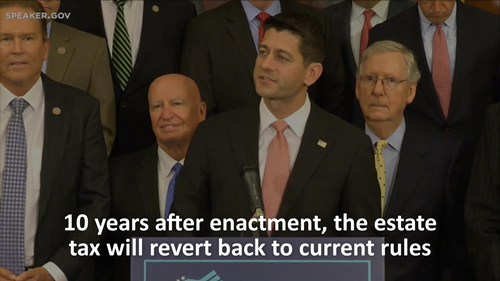

The elimination of the estate tax is proposed, but it would only be eliminated temporarily - for 10 years.

Under the proposal, estate tax laws would revert back to current rules a decade after enactment.

Click image to enlarge

It's only prudent to plan for the reforms to become effective January 1st, 2018.

This may seem defensive but it's just good planning.

Click image to enlarge

We are independent financial advisors, a source of objective, authoritative facts about wealth management.

We'll have updates on year-end tax planning in the weeks ahead.

Please subscribe to our e-mail newsletter to see our reports on your smartphone.

Click image to enlarge